India’s property market has started 2026 on a confident and steady note. Indian real estate investment hit USD 1.6 billion in the first quarter of 2026, showing that large investors and institutions continue to back this sector even when the global environment feels uncertain. To put it in simpler terms, more than one lakh crore rupees flowed into Indian property markets in just three months.

Even though the total amount was slightly lower compared to the previous quarter, it stood 64% higher than the average first-quarter investment recorded since 2020. That comparison matters a great deal. It shows how far India’s investment story has come and how much stronger the foundation has become. The market is not just recovering. It is building on something real.

This blog draws on data published by Colliers India for Q1 2026. The goal is to help real estate investors understand where the money is coming from, where it is going, and what it all means for the market going forward.

Table of Contents

Domestic Investors Are Now Leading Indian Real Estate Investment

For the first time in a significant way, Indian investors are clearly driving the market forward. This shift is one of the most important stories coming out of Q1 2026, and it deserves a closer look.

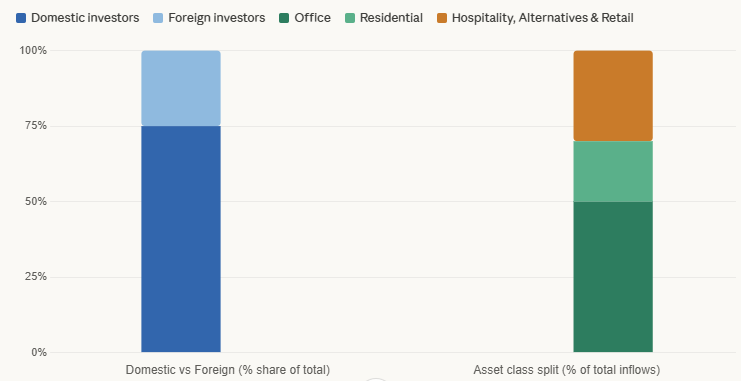

Total domestic inflows reached USD 1.2 billion this quarter, accounting for 75% of all capital that entered Indian real estate investment during this period. On a year-on-year basis, this marks a 57% jump compared to the same quarter last year. Historically, domestic investors used to contribute between 20% and 50% of total inflows. Crossing the 75% mark is a meaningful milestone for the sector.

Badal Yagnik, CEO and MD of Colliers India, pointed out that this surge in domestic participation reflects growing confidence among Indian institutional players. He noted that India’s young population, strong consumer economy, and expanding appetite for both traditional and newer asset classes continue to give the country a strong position within the Asia-Pacific investment region.

Why This Shift Makes the Market More Stable

When domestic capital leads, the market becomes far less dependent on what happens globally. If foreign investors pull back due to international uncertainty, local money fills the gap and keeps the momentum going. This is exactly what happened in Q1 2026. It is a healthy sign that Indian real estate investment is maturing and standing on its own feet.

The chart above shows two things clearly: domestic capital is dominating the source of funds this quarter, and office remains the single largest asset class by a wide margin.

Foreign Inflows Slow Down, But Context Is Everything

Foreign inflows came in at USD 0.4 billion for the quarter, a decline of 23% compared to Q1 2025. The main reason is the uncertain global environment, including volatility in trade policies, crude oil, and commodity markets. When global conditions become unpredictable, large foreign funds tend to be more careful about where they place their money.

However, this does not mean foreign investors have lost interest in Indian real estate investment. They are still participating, but more selectively. This quarter, most of their capital went into hospitality and alternative asset classes, where the balance between risk and return fits their investment goals well. The broader case for India remains intact. The caution is driven by external factors, not by anything specific to India.

Breaking Down the Numbers: Where Indian Real Estate Investment Is Going

Understanding where the money went is just as important as knowing how much came in. Different asset types attracted very different levels of interest this quarter, and the pattern reveals some clear trends.

Office Spaces Lead, Residential Holds Steady

The office sector attracted the largest share, pulling in USD 0.8 billion, which is 50% of total inflows and nearly double the amount office assets received in Q1 2025. Companies continue to lease and expand Grade A office spaces across major cities, and investors are backing that demand with conviction. Notably, more than 90% of this investment came from domestic investors, showing strong local confidence in commercial real estate.

Residential assets came in second, receiving USD 0.3 billion or 20% of total inflows. Housing demand in India’s top cities has stayed strong for several quarters, and investors continue to support residential projects, especially in the mid-to-premium segment.

Key figures at a glance:

- Office assets: 50% of total inflows, nearly double Q1 2025 levels, with domestic investors accounting for over 90% of this segment

- Residential assets: 20% of total inflows, reflecting sustained housing demand

- Hospitality, alternatives, and retail combined: over 20% of total inflows, with foreign capital taking a 70% share within this group

- Multi-city investment deals: nearly USD 0.5 billion, with hospitality and residential making up roughly two-thirds of these transactions

Hospitality and Alternatives Are Gaining Real Ground

Beyond office and residential, there is a growing story in hospitality, alternative assets, and retail. Together, these segments attracted more than USD 0.35 billion this quarter, contributing over 20% of total Indian real estate investment flows.

Foreign investors played a dominant role here, contributing around 70% of the capital flowing into these categories. Hotels, data centres, warehousing, and other alternative formats are becoming increasingly attractive to global funds looking to diversify beyond traditional commercial and housing assets.

Foreign capital diversifying into these newer categories signals that India is being recognized as a market capable of supporting a wider range of real estate investment opportunities.

For everyday investors and market observers, authorized investment platforms help track these sector-level shifts and show how broader investment trends connect to ground-level property developments across cities.

Delhi NCR and Bengaluru Lead the Geographic Picture

Among individual cities, Delhi NCR and Bengaluru together accounted for 46% of total inflows this quarter. Delhi NCR attracted around USD 0.4 billion or roughly 25% of the total, while Bengaluru drew approximately USD 0.3 billion. These two cities continue to anchor investor preference, driven by deep office demand, growing residential activity, and ongoing infrastructure upgrades.

The remaining investment spread across multiple cities through multi-city deal structures totalling nearly USD 0.5 billion. This shows that Indian real estate investment appetite is gradually widening beyond just the top two markets toward cities that offer differentiated demand stories in residential and hospitality.

Institutional Investment Volumes Are Rising, and That Matters

Overall institutional investment volumes in Indian real estate rose 25% year-on-year in Q1 2026. Institutional investors are large, organised entities such as real estate funds, insurance companies, and listed platforms that deploy capital through structured, professionally managed deals. When their participation grows, it typically signals that the market is becoming more transparent, better governed, and more accessible to a wider range of participants.

This 25% year-on-year growth, combined with Q1 volumes sitting 64% above the post-2020 average, reflects a market that has built genuine depth. Investors are making informed, long-term commitments based on fundamentals, not short-term enthusiasm.

What This All Means for the Road Ahead

The Q1 2026 data does not present a market running hot or overheated. It presents something more valuable: a market that is steady, resilient, and growing on the back of real demand.

A few clear takeaways stand out from this quarter:

- Domestic investors now form the backbone of Indian real estate investment, making the market more insulated from global volatility

- The office sector has made a strong comeback, with investment nearly doubling year-on-year

- Alternative and hospitality segments are emerging as serious categories, particularly for foreign capital seeking diversification

- Multi-city deals show that the growth story is slowly becoming broader and more inclusive of Tier 2 and emerging markets

Foreign investor caution is a real factor right now, but it is driven by global macro pressures rather than any fundamental concern about India. As those external conditions stabilise, foreign participation in Indian real estate investment is likely to recover.

Conclusion:

India’s real estate market in Q1 2026 demonstrates exactly the kind of resilience that long-term investors look for. Domestic capital is strong, institutional participation is growing, asset classes are diversifying, and the overall investment volume remains well above historical averages.

This blog is purely informational. The data referenced here comes from Colliers India’s Q1 2026 research. For those who want to verify figures or explore deeper analysis, Colliers’ official quarterly report, along with platforms such as ANAROCK and Cushman & Wakefield, are reliable references for cross-checking market data.